7. Financing of Constructed Facilities7.1 The Financing ProblemInvestment in a constructed facility represents a cost in the short term that returns benefits only over the long term use of the facility. Thus, costs occur earlier than the benefits, and owners of facilities must obtain the capital resources to finance the costs of construction. A project cannot proceed without adequate financing, and the cost of providing adequate financing can be quite large. For these reasons, attention to project finance is an important aspect of project management. Finance is also a concern to the other organizations involved in a project such as the general contractor and material suppliers. Unless an owner immediately and completely covers the costs incurred by each participant, these organizations face financing problems of their own. At a more general level, project finance is only one aspect of the general problem of corporate finance. If numerous projects are considered and financed together, then the net cash flow requirements constitutes the corporate financing problem for capital investment. Whether project finance is performed at the project or at the corporate level does not alter the basic financing problem. In essence, the project finance problem is to obtain funds to bridge the time between making expenditures and obtaining revenues. Based on the conceptual plan, the cost estimate and the construction plan, the cash flow of costs and receipts for a project can be estimated. Normally, this cash flow will involve expenditures in early periods. Covering this negative cash balance in the most beneficial or cost effective fashion is the project finance problem. During planning and design, expenditures of the owner are modest, whereas substantial costs are incurred during construction. Only after the facility is complete do revenues begin. In contrast, a contractor would receive periodic payments from the owner as construction proceeds. However, a contractor also may have a negative cash balance due to delays in payment and retainage of profits or cost reimbursements on the part of the owner. Plans considered by owners for facility financing typically have both long and short term aspects. In the long term, sources of revenue include sales, grants, and tax revenues. Borrowed funds must be eventually paid back from these other sources. In the short term, a wider variety of financing options exist, including borrowing, grants, corporate investment funds, payment delays and others. Many of these financing options involve the participation of third parties such as banks or bond underwriters. For private facilities such as office buildings, it is customary to have completely different financing arrangements during the construction period and during the period of facility use. During the latter period, mortgage or loan funds can be secured by the value of the facility itself. Thus, different arrangements of financing options and participants are possible at different stages of a project, so the practice of financial planning is often complicated. On the other hand, the options for borrowing by contractors to bridge their expenditures and receipts during construction are relatively limited. For small or medium size projects, overdrafts from bank accounts are the most common form of construction financing. Usually, a maximum limit is imposed on an overdraft account by the bank on the basis of expected expenditures and receipts for the duration of construction. Contractors who are engaged in large projects often own substantial assets and can make use of other forms of financing which have lower interest charges than overdrafting. In this chapter, we will first consider facility financing from the owner's perspective, with due consideration for its interaction with other organizations involved in a project. Later, we discuss the problems of construction financing which are crucial to the profitability and solvency of construction contractors. Back to top7.2 Institutional Arrangements for Facility FinancingFinancing arrangements differ sharply by type of owner and by the type of facility construction. As one example, many municipal projects are financed in the United States with tax exempt bonds for which interest payments to a lender are exempt from income taxes. As a result, tax exempt municipal bonds are available at lower interest charges. Different institutional arrangements have evolved for specific types of facilities and organizations. A private corporation which plans to undertake large capital projects may use its retained earnings, seek equity partners in the project, issue bonds, offer new stocks in the financial markets, or seek borrowed funds in another fashion. Potential sources of funds would include pension funds, insurance companies, investment trusts, commercial banks and others. Developers who invest in real estate properties for rental purposes have similar sources, plus quasi-governmental corporations such as urban development authorities. Syndicators for investment such as real estate investment trusts (REITs) as well as domestic and foreign pension funds represent relatively new entries to the financial market for building mortgage money. Public projects may be funded by tax receipts, general revenue bonds, or special bonds with income dedicated to the specified facilities. General revenue bonds would be repaid from general taxes or other revenue sources, while special bonds would be redeemed either by special taxes or user fees collected for the project. Grants from higher levels of government are also an important source of funds for state, county, city or other local agencies. Despite the different sources of borrowed funds, there is a rough equivalence in the actual cost of borrowing money for particular types of projects. Because lenders can participate in many different financial markets, they tend to switch towards loans that return the highest yield for a particular level of risk. As a result, borrowed funds that can be obtained from different sources tend to have very similar costs, including interest charges and issuing costs. As a general principle, however, the costs of funds for construction will vary inversely with the risk of a loan. Lenders usually require security for a loan represented by a tangible asset. If for some reason the borrower cannot repay a loan, then the borrower can take possession of the loan security. To the extent that an asset used as security is of uncertain value, then the lender will demand a greater return and higher interest payments. Loans made for projects under construction represent considerable risk to a financial institution. If a lender acquires an unfinished facility, then it faces the difficult task of re-assembling the project team. Moreover, a default on a facility may result if a problem occurs such as foundation problems or anticipated unprofitability of the future facility. As a result of these uncertainties, construction lending for unfinished facilities commands a premium interest charge of several percent compared to mortgage lending for completed facilities. Financing plans will typically include a reserve amount to cover unforeseen expenses, cost increases or cash flow problems. This reserve can be represented by a special reserve or a contingency amount in the project budget. In the simplest case, this reserve might represent a borrowing agreement with a financial institution to establish a line of credit in case of need. For publicly traded bonds, specific reserve funds administered by a third party may be established. The cost of these reserve funds is the difference between the interest paid to bondholders and the interest received on the reserve funds plus any administrative costs. Finally, arranging financing may involve a lengthy period of negotiation and review. Particularly for publicly traded bond financing, specific legal requirements in the issue must be met. A typical seven month schedule to issue revenue bonds would include the various steps outlined in Table 7-1. [1] In many cases, the speed in which funds may be obtained will determine a project's financing mechanism.

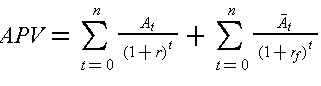

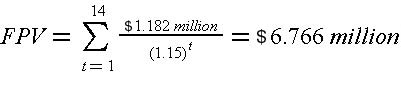

Example 7-1: Example of financing options Suppose that you represent a private corporation attempting to arrange financing for a new headquarters building. These are several options that might be considered:Back to top 7.3 Evaluation of Alternative Financing PlansSince there are numerous different sources and arrangements for obtaining the funds necessary for facility construction, owners and other project participants require some mechanism for evaluating the different potential sources. The relative costs of different financing plans are certainly important in this regard. In addition, the flexibility of the plan and availability of reserves may be critical. As a project manager, it is important to assure adequate financing to complete a project. Alternative financing plans can be evaluated using the same techniques that are employed for the evaluation of investment alternatives. As described in Chapter 6, the availability of different financing plans can affect the selection of alternative projects. A general approach for obtaining the combined effects of operating and financing cash flows of a project is to determine the adjusted net present value (APV) which is the sum of the net present value of the operating cash flow (NPV) and the net present value of the financial cash flow (FPV), discounted at their respective minimum attractive rates of return (MARR), i.e.,

where r is the MARR reflecting the risk of the operating cash flow and rf is the MARR representing the cost of borrowing for the financial cash flow. Thus,

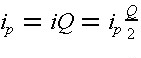

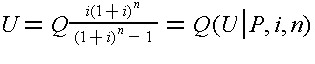

where At and For the sake of simplicity, we shall emphasize in this chapter the evaluation of financing plans, with occasional references to the combined effects of operating and financing cash flows. In all discussions, we shall present various financing schemes with examples limiting to cases of before-tax cash flows discounted at a before-tax MARR of r = rf for both operating and financial cash flows. Once the basic concepts of various financing schemes are clearly understood, their application to more complicated situations involving depreciation, tax liability and risk factors can be considered in combination with the principles for dealing with such topics enunciated in Chapter 6. In this section, we shall concentrate on the computational techniques associated with the most common types of financing arrangements. More detailed descriptions of various financing schemes and the comparisons of their advantages and disadvantages will be discussed in later sections. Typically, the interest rate for borrowing is stated in terms of annual percentage rate (A.P.R.), but the interest is accrued according to the rate for the interest period specified in the borrowing agreement. Let ip be the nominal annual percentage rate, and i be the interest rate for each of the p interest periods per year. By definition

If interest is accrued semi-annually, i.e., p = 2, the interest rate per period is ip/2; similarly if the interest is accrued monthly, i.e., p = 12, the interest rate per period is ip/12. On the other hand, the effective annual interest rate ie is given by:

Note that the effective annual interest rate, ie, takes into account compounding within the year. As a result, ie is greater than ip for the typical case of more than one compounding period per year. For a coupon bond, the face value of the bond denotes the amount borrowed (called principal) which must be repaid in full at a maturity or due date, while each coupon designates the interest to be paid periodically for the total number of coupons covering all periods until maturity. Let Q be the amount borrowed, and Ip be the interest payment per period which is often six months for coupon bonds. If the coupon bond is prescribed to reach maturity in n years from the date of issue, the total number of interest periods will be pn = 2n. The semi-annual interest payment is given by:

In purchasing a coupon bond, a discount from or a premium above the face value may be paid. An alternative loan arrangement is to make a series of uniform payments including both interest and part of the principal for a pre-defined number of repayment periods. In the case of uniform payments at an interest rate i for n repayment periods, the uniform repayment amount U is given by:

where (U|P,i,n) is a capital recovery factor which reads: "to find U, given P=1, for an interest rate i over n periods." Compound interest factors are as tabulated in Appendix A. The number of repayment periods n will clearly influence the amounts of payments in this uniform payment case. Uniform payment bonds or mortgages are based on this form of repayment. Usually, there is an origination fee associated with borrowing for legal and other professional services which is payable upon the receipt of the loan. This fee may appear in the form of issuance charges for revenue bonds or percentage point charges for mortgages. The borrower must allow for such fees in addition to the construction cost in determining the required original amount of borrowing. Suppose that a sum of Po must be reserved at t=0 for the construction cost, and K is the origination fee. Then the original loan needed to cover both is:

If the origination fee is expressed as k percent of the original loan, i.e., K = kQ0, then:

Since interest and sometimes parts of the principal must be repaid periodically

in most financing arrangements, an amount Q considerably larger than Q0

is usually borrowed in the beginning to provide adequate reserve funds

to cover interest payments, construction cost increases and other unanticipated

shortfalls. The net amount received from borrowing is deposited in a separate

interest bearing account from which funds will be withdrawn periodically

for necessary payments. Let the borrowing rate per period be denoted by

i and the interest for the running balance accrued to the project reserve

account be denoted by h. Let At be the net operating cash flow

for - period t (negative for construction cost in period t) and

where the value of At or t may be zero for some period(s). Equations (7.9) and (7.10) are approximate in that interest might be earned on intermediate balances based on the pattern of payments during a period instead of at the end of a period. Because the borrowing rate i will generally exceed the investment rate h for the running balance in the project account and since the origination fee increases with the amount borrowed, the financial planner should minimize the amount of money borrowed under this finance strategy. Thus, there is an optimal value for Q such that all estimated shortfalls are covered, interest payments and expenses are minimized, and adequate reserve funds are available to cover unanticipated factors such as construction cost increases. This optimal value of Q can either be identified analytically or by trial and error. Finally, variations in ownership arrangements may also be used to provide at least partial financing. Leasing a facility removes the need for direct financing of the facility. Sale-leaseback involves sale of a facility to a third party with a separate agreement involving use of the facility for a pre-specified period of time. In one sense, leasing arrangements can be viewed as a particular form of financing. In return for obtaining the use of a facility or piece of equipment, the user (lesser) agrees to pay the owner (lesser) a lease payment every period for a specified number of periods. Usually, the lease payment is at a fixed level due every month, semi-annually, or annually. Thus, the cash flow associated with the equipment or facility use is a series of uniform payments. This cash flow would be identical to a cash flow resulting from financing the facility or purchase with sufficient borrowed funds to cover initial construction (or purchase) and with a repayment schedule of uniform amounts. Of course, at the end of the lease period, the ownership of the facility or equipment would reside with the lesser. However, the lease terms may include a provision for transferring ownership to the lesser after a fixed period. Example 7-2: A coupon bond cash flow and cost A private corporation wishes to borrow $10.5 million for the construction of a new building by issuing a twenty-year coupon bond at an annual percentage interest rate of 10% to be paid semi-annually, i.e. 5% per interest period of six months. The principal will be repaid at the end of 20 years. The amount borrowed will cover the construction cost of $10.331 million and an origination fee of $169,000 for issuing the coupon bond. Example 7-3: An example of leasing versus ownership analysis Suppose that a developer offered a building to a corporation for an annual lease payment of $10 million over a thirty year lifetime. For the sake of simplicity, let us assume that the developer also offers to donate the building to the corporation at the end of thirty years or, alternatively, the building would then have no commercial value. Also, suppose that the initial cost of the building was $65.66 million. For the corporation, the lease is equivalent to receiving a loan with uniform payments over thirty years at an interest rate of 15% since the present value of the lease payments is equal to the initial cost at this interest rate: Example 7-4: Example evaluation of alternative financing plans. Suppose that a small corporation wishes to build a headquarters building. The construction will require two years and cost a total of $12 million, assuming that $5 million is spent at the end of the first year and $7 million at the end of the second year. To finance this construction, several options are possible, including:

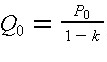

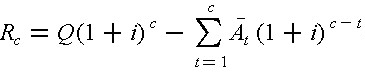

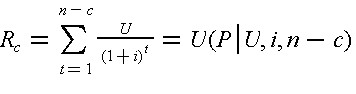

7.4 Secured Loans with Bonds, Notes and MortgagesSecured lending involves a contract between a borrower and lender, where the lender can be an individual, a financial institution or a trust organization. Notes and mortgages represent formal contracts between financial institutions and owners. Usually, repayment amounts and timing are specified in the loan agreement. Public facilities are often financed by bond issues for either specific projects or for groups of projects. For publicly issued bonds, a trust company is usually designated to represent the diverse bond holders in case of any problems in the repayment. The borrowed funds are usually secured by granting the lender some rights to the facility or other assets in case of defaults on required payments. In contrast, corporate bonds such as debentures can represent loans secured only by the good faith and credit worthiness of the borrower. Under the terms of many bond agreements, the borrower reserves the right

to repurchase the bonds at any time before the maturity date by repaying

the principal and all interest up to the time of purchase. The required

repayment Rc at the end of period c is the net future value

of the borrowed amount Q - less the payment

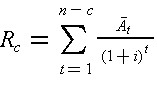

The required repayment Rc at the end of the period c can also be obtained by noting the net present value of the repayments in the remaining (n-c) periods discounted at the borrowing rate i to t = c as follows:

For coupon bonds, the required repayment Rc after the redemption of the coupon at the end of period c is simply the original borrowed amount Q. For uniform payment bonds, the required repayment Rc after the last payment at the end of period c is:

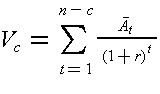

Many types of bonds can be traded in a secondary market by the bond holder. As interest rates fluctuate over time, bonds will gain or lose in value. The actual value of a bond is reflected in the market discount or premium paid relative to the original principal amount (the face value). Another indicator of this value is the yield to maturity or internal rate of return of the bond. This yield is calculated by finding the interest rate that sets the (discounted) future cash flow of the bond equal to the current market price:

where Vc is the current market value after c periods have

lapsed since the - issuance of the bond, Several other factors come into play in evaluation of bond values from the lenders point of view, however. First, the lender must adjust for the possibility that the borrower may default on required interest and principal payments. In the case of publicly traded bonds, special rating companies divide bonds into different categories of risk for just this purpose. Obviously, bonds that are more likely to default will have a lower value. Secondly, lenders will typically make adjustments to account for changes in the tax code affecting their after-tax return from a bond. Finally, expectations of future inflation or deflation as well as exchange rates will influence market values. Another common feature in borrowing agreements is to have a variable interest rate. In this case, interest payments would vary with the overall market interest rate in some pre-specified fashion. From the borrower's perspective, this is less desirable since cash flows are less predictable. However, variable rate loans are typically available at lower interest rates because the lenders are protected in some measure from large increases in the market interest rate and the consequent decrease in value of their expected repayments. Variable rate loans can have floors and ceilings on the applicable interest rate or on rate changes in each year. Example 7-5: Example of a corporate promissory note A corporation wishes to consider the option of financing the headquarters building in Example 7-4 by issuing a five year promissory note which requires an origination fee for the note is $25,000. Then a total borrowed amount needed at the beginning of the first year to pay for the construction costs and origination fee is 10.331 + 0.025 = $10.356 million. Interest payments are made annually at an annual rate of 10.8% with repayment of the principal at the end of the fifth year. Thus, the annual interest payment is (10.8%)(10.356) = $1.118 million. With the data in Example 7-4 for construction costs and accrued interests for the first two year, the combined operating and and financial cash flows in million dollars can be obtained:Year 0, AA0 = 10.356 - 0.025 = 10.331At the current corporate MARR of 15%, Example 7-6: Bond financing mechanisms. Suppose that the net operating expenditures and receipts of a facility investment over a five year time horizon are as shown in column 2 of Table 7-3 in which each period is six months. This is a hypothetical example with a deliberately short life time period to reduce the required number of calculations. Consider two alternative bond financing mechanisms for this project. Both involve borrowing $2.5 million at an issuing cost of five percent of the loan with semi-annual repayments at a nominal annual interest rate of ten percent i.e., 5% per period. Any excess funds can earn an interest of four percent each semi-annual period. The coupon bond involves only interest payments in intermediate periods, plus the repayment of the principal at the end, whereas the uniform payment bond requires ten uniform payments to cover both interests and the principal. Both bonds are subject to optional redemption by the borrower before maturity.

Example 7-7: Provision of Reserve Funds Typical borrowing agreements may include various required reserve funds. [2] Consider an eighteen month project costing five million dollars. To finance this facility, coupon bonds will be issued to generate revenues which must be sufficient to pay interest charges during the eighteen months of construction, to cover all construction costs, to pay issuance expenses, and to maintain a debt service reserve fund. The reserve fund is introduced to assure bondholders of payments in case of unanticipated construction problems. It is estimated that a total amount of $7.4 million of bond proceeds is required, including a two percent discount to underwriters and an issuance expense of $100,000.

Example 7-8: Variable rate revenue bonds prospectus The information in Table 7-5 is abstracted from the Prospectus for a new issue of revenue bonds for the Atwood City. This prospectus language is typical for municipal bonds. Notice the provision for variable rate after the initial interest periods. The borrower reserves the right to repurchase the bond before the date for conversion to variable rate takes effect in order to protect itself from declining market interest rates in the future so that the borrower can obtain other financing arrangements at lower rates.

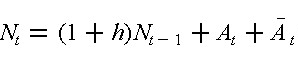

Back to top 7.5 Overdraft AccountsOverdrafts can be arranged with a banking institution to allow accounts to have either a positive or a negative balance. With a positive balance, interest is paid on the account balance, whereas a negative balance incurs interest charges. Usually, an overdraft account will have a maximum overdraft limit imposed. Also, the interest rate h available on positive balances is less than the interest rate i charged for borrowing. Clearly, the effects of overdraft financing depends upon the pattern of cash flows over time. Suppose that the net cash flow for period t in the account is denoted by At which is the difference between the receipt Pt and the payment Et in period t. Hence, At can either be positive or negative. The amount of overdraft at the end of period t is the cumulative net cash flow Nt which may also be positive or negative. If Nt is positive, a surplus is indicated and the subsequent interest would be paid to the borrower. Most often, Nt is negative during the early time periods of a project and becomes positive in the later periods when the borrower has received payments exceeding expenses. If the borrower uses overdraft financing and pays the interest per period on the accumulated overdraft at a borrowing rate i in each period, then the interest per period for the accumulated overdraft Nt-1 from the previous period (t-1) is It = iNt-1 where It would be negative for a negative account balance Nt-1. For a positive account balance, the interest received is It = hNt-1 where It would be positive for a positive account balance. The account balance Nt at each period t is the sum of receipts Pt, payments Et, interest It and the account balance from the previous period Nt-1. Thus,

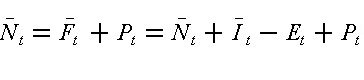

where It = iNt-1 for a negative Nt-1 and It = hNt-1 for a positive Nt-1. The net cash flow At = Pt - Et is positive for a net receipt and negative for a net payment. This equation is approximate in that the interest might be earned on intermediate balances based on the pattern of payments during the period instead of at the end of a period. The account balance in each period is of interest because there will always be a maximum limit on the amount of overdraft available. For the purpose of separating project finances with other receipts and payments in an organization, it is convenient to establish a credit account into which receipts related to the project must be deposited when they are received, and all payments related to the project will be withdrawn from this account when they are needed. Since receipts typically lag behind payments for a project, this credit account will have a negative balance until such time when the receipts plus accrued interests are equal to or exceed payments in the period. When that happens, any surplus will not be deposited in the credit account, and the account is then closed with a zero balance. In that case, for negative Nt-1, Eq. (7.15) can be expressed as:

and as soon as Nt reaches a positive value or zero, the account is closed. Example 7-9: Overdraft Financing with Grants to a Local Agency A public project which costs $61,525,000 is funded eighty percent by a federal grant and twenty percent from a state grant. The anticipated duration of the project is six years with receipts from grant funds allocated at the end of each year to a local agency to cover partial payments to contractors for that year while the remaining payments to contractors will be allocated at the end of the sixth year. The end-of-year payments are given in Table 7-6 in which t=0 refers to the beginning of the project, and each period is one year.

Example 7-10: Use of overdraft financing for a facility A corporation is contemplating an investment in a facility with the following before-tax operating net cash flow (in thousands of dollars) at year ends:

Back on top 7.6 Refinancing of DebtsRefinancing of debts has two major advantages for an owner. First, they allow re-financing at intermediate stages to save interest charges. If a borrowing agreement is made during a period of relatively high interest charges, then a repurchase agreement allows the borrower to re-finance at a lower interest rate. Whenever the borrowing interest rate declines such that the savings in interest payments will cover any transaction expenses (for purchasing outstanding notes or bonds and arranging new financing), then it is advantageous to do so. Another reason to repurchase bonds is to permit changes in the operation of a facility or new investments. Under the terms of many bond agreements, there may be restrictions on the use of revenues from a particular facility while any bonds are outstanding. These restrictions are inserted to insure bondholders that debts will be repaid. By repurchasing bonds, these restrictions are removed. For example, several bridge authorities had bonds that restricted any diversion of toll revenues to other transportation services such as transit. By repurchasing these bonds, the authority could undertake new operations. This type of repurchase may occur voluntarily even without a repurchase agreement in the original bond. The borrower may give bondholders a premium to retire bonds early. Example 7-11: Refinancing a loan. Suppose that the bank loan shown in Example 7-4 had a provision permitting the borrower to repay the loan without penalty at any time. Further, suppose that interest rates for new loans dropped to nine percent at the end of year six of the loan. Issuing costs for a new loan would be $50,000. Would it be advantageous to re-finance the loan at that time?Back to top 7.7 Project versus Corporate FinanceWe have focused so far on problems and concerns at the project level. While this is the appropriate viewpoint for project managers, it is always worth bearing in mind that projects must fit into broader organizational decisions and structures. This is particularly true for the problem of project finance, since it is often the case that financing is planned on a corporate or agency level, rather than a project level. Accordingly, project managers should be aware of the concerns at this level of decision making. A construction project is only a portion of the general capital budgeting problem faced by an owner. Unless the project is very large in scope relative to the owner, a particular construction project is only a small portion of the capital budgeting problem. Numerous construction projects may be lumped together as a single category in the allocation of investment funds. Construction projects would compete for attention with equipment purchases or other investments in a private corporation. Financing is usually performed at the corporate level using a mixture of long term corporate debt and retained earnings. A typical set of corporate debt instruments would include the different bonds and notes discussed in this chapter. Variations would typically include different maturity dates, different levels of security interests, different currency denominations, and, of course, different interest rates. Grouping projects together for financing influences the type of financing that might be obtained. As noted earlier, small and large projects usually involve different institutional arrangements and financing arrangements. For small projects, the fixed costs of undertaking particular kinds of financing may be prohibitively expensive. For example, municipal bonds require fixed costs associated with printing and preparation that do not vary significantly with the size of the issue. By combining numerous small construction projects, different financing arrangements become more practical. While individual projects may not be considered at the corporate finance level, the problems and analysis procedures described earlier are directly relevant to financial planning for groups of projects and other investments. Thus, the net present values of different financing arrangements can be computed and compared. Since the net present values of different sub-sets of either investments or financing alternatives are additive, each project or finance alternative can be disaggregated for closer attention or aggregated to provide information at a higher decision making level. Example 7-12: Basic types of repayment schedules for loans.

Back to top 7.8 Shifting Financial BurdensThe different participants in the construction process have quite distinct perspectives on financing. In the realm of project finance, the revenues to one participant represent an expenditure to some other participant. Payment delays from one participant result in a financial burden and a cash flow problem to other participants. It is common occurrence in construction to reduce financing costs by delaying payments in just this fashion. Shifting payment times does not eliminate financing costs, however, since the financial burden still exists. Traditionally, many organizations have used payment delays both to shift financing expenses to others or to overcome momentary shortfalls in financial resources. From the owner's perspective, this policy may have short term benefits, but it certainly has long term costs. Since contractors do not have large capital assets, they typically do not have large amounts of credit available to cover payment delays. Contractors are also perceived as credit risks in many cases, so loans often require a premium interest charge. Contractors faced with large financing problems are likely to add premiums to bids or not bid at all on particular work. For example, A. Maevis noted: [3]

Even after bids are received and contracts signed, delays in payments may form the basis for a successful claim against an agency on the part of the contractor. The owner of a constructed facility usually has a better credit rating and can secure loans at a lower borrowing rate, but there are some notable exceptions to this rule, particularly for construction projects in developing countries. Under certain circumstances, it is advisable for the owner to advance periodic payments to the contractor in return for some concession in the contract price. This is particularly true for large-scale construction projects with long durations for which financing costs and capital requirements are high. If the owner is willing to advance these amounts to the contractor, the gain in lower financing costs can be shared by both parties through prior agreement. Unfortunately, the choice of financing during the construction period is often left to the contractor who cannot take advantage of all available options alone. The owner is often shielded from participation through the traditional method of price quotation for construction contracts. This practice merely exacerbates the problem by excluding the owner from participating in decisions which may reduce the cost of the project. Under conditions of economic uncertainty, a premium to hedge the risk must be added to the estimation of construction cost by both the owner and the contractor. The larger and longer the project is, the greater is the risk. For an unsophisticated owner who tries to avoid all risks and to place the financing burdens of construction on the contractor, the contract prices for construction facilities are likely to be increased to reflect the risk premium charged by the contractors. In dealing with small projects with short durations, this practice may be acceptable particularly when the owner lacks any expertise to evaluate the project financing alternatives or the financial stability to adopt innovative financing schemes. However, for large scale projects of long duration, the owner cannot escape the responsibility of participation if it wants to avoid catastrophes of run-away costs and expensive litigation. The construction of nuclear power plants in the private sector and the construction of transportation facilities in the public sector offer ample examples of such problems. If the responsibilities of risk sharing among various parties in a construction project can be clearly defined in the planning stage, all parties can be benefited to take advantage of cost saving and early use of the constructed facility. Example 7-13: Effects of payment delays Table 7-9 shows an example of the effects of payment timing on the general contractor and subcontractors. The total contract price for this project is $5,100,000 with scheduled payments from the owner shown in Column 2. The general contractor's expenses in each period over the lifetime of the project are given in Column 3 while the subcontractor's expenses are shown in Column 4. If the general contractor must pay the subcontractor's expenses as well as its own at the end of each period, the net cash flow of the general contractor is obtained in Column 5, and its cumulative cash flow in Column 6.

Back to top 7.9 Construction Financing for ContractorsFor a general contractor or subcontractor, the cash flow profile of expenses and incomes for a construction project typically follows the work in progress for which the contractor will be paid periodically. The markup by the contractor above the estimated expenses is included in the total contract price and the terms of most contracts generally call for monthly reimbursements of work completed less retainage. At time period 0, which denotes the beginning of the construction contract, a considerable sum may have been spent in preparation. The contractor's expenses which occur more or less continuously for the project duration are depicted by a piecewise continuous curve while the receipts (such as progress payments from the owner) are represented by a step function as shown in Fig. 7-1. The owner's payments for the work completed are assumed to lag one period behind expenses except that a withholding proportion or remainder is paid at the end of construction. This method of analysis is applicable to realistic situations where a time period is represented by one month and the number of time periods is extended to cover delayed receipts as a result of retainage.

Figure 7-1 Contractor's Expenses and Owner's Payments While the cash flow profiles of expenses and receipts are expected to

vary for different projects, the characteristics of the curves depicted

in Fig. 7-1 are sufficiently general for most cases. Let Et

represent the contractor's expenses in period t, and Pt represent

owner's payments in period t, for t=0,1,2,...,n for n=5 in this case.

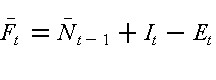

The net operating cash flow at the end of period t for t

where At is positive for a surplus and negative for a shortfall. The cumulative operating cash flow at the end of period t just before

receiving payment Pt (for t

where Nt-1 is the cumulative net cash flows from period 0

to period (t-1). Furthermore, the cumulative net operating cash flow after

receiving payment Pt at the end of period t (for t

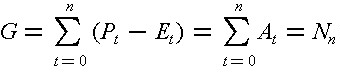

The gross operating profit G for a n-period project is defined as net operating cash flow at t=n and is given by:

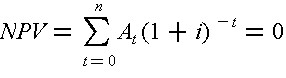

The use of Nn as a measure of the gross operating profit has the disadvantage that it is not adjusted for the time value of money. Since the net cash flow At (for t=0,1,...,n) for a construction project represents the amount of cash required or accrued after the owner's payment is plowed back to the project at the end of period t, the internal rate of return (IRR) of this cash flow is often cited in the traditional literature in construction as a profit measure. To compute IRR, let the net present value (NPV) of At discounted at a discount rate i per period be zero, i.e.,

The resulting i (if it is unique) from the solution of Eq. (7.21) is the IRR of the net cash flow At. Aside from the complications that may be involved in the solution of Eq. (7.21), the resulting i = IRR has a meaning to the contractor only if the firm finances the entire project from its own equity. This is seldom if ever the case since most construction firms are highly leveraged, i.e. they have relatively small equity in fixed assets such as construction equipment, and depend almost entirely on borrowing in financing individual construction projects. The use of the IRR of the net cash flows as a measure of profit for the contractor is thus misleading. It does not represent even the IRR of the bank when the contractor finances the project through overdraft since the gross operating profit would not be given to the bank. Since overdraft is the most common form of financing for small or medium

size projects, we shall consider the financing costs and effects on profit

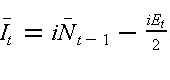

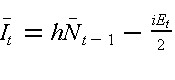

of - the use of overdrafts. Let The inclusion of enterest on contractor's expenses Et during

period t (for G 1) is based on the rationale that the S-shaped curve depicting

the contractor's expenses in Figure 7-1 is fairly typical of actual situations,

where the owner's payments are typically made at the end of well defined

periods. Hence, interest on expenses during period t is approximated by

one half of the amount as if the expenses were paid at the beginning of

the period. In fact, Et is the accumulation of all expenses

in period t and is treated - as an expense at the end of the period. Thus,

the interest per period

Hence, if the cumulative net cash flow Including the interest accrued in period t, the cumulative cash flow

at the end of period t just before receiving payment Pt (for

t

Furthermore, the cumulative net cash flow after receiving payment Pt

at the end of period t (for t

The gross operating profit

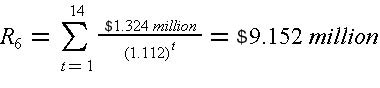

where Example 7-14: Contractor's gross profit from a project The contractor's expenses and owner's payments for a multi-year construction project are given in Columns 2 and 3, respectively, of Table 7-11. Each time period is represented by one year, and the annual interest rate i is for borrowing 11%. The computation has been carried out in Table 7-11, and the contractor's gross profit G is found to be N5 = $8.025 million in the last column of the table.

Example 7-15: Effects of Construction Financing The computation of the cumulative cash flows including interest charges at i = 11% for Example 7-14 is shown in Table 7-12 with gross profit

Figure 7-2 Effects of Overdraft Financing Back to top 7.10 Effects of Other Factors on a Contractor's ProfitsIn times of economic uncertainty, the fluctuations in inflation rates and market interest rates affect profits significantly. The total contract price is usually a composite of expenses and payments in then-current dollars at different payment periods. In this case, estimated expenses are also expressed in then-current dollars. During periods of high inflation, the contractor's profits are particularly vulnerable to delays caused by uncontrollable events for which the owner will not be responsible. Hence, the owner's payments will not be changed while the contractor's expenses will increase with inflation. Example 7-16: Effects of Inflation Suppose that both expenses and receipts for the construction project in the Example 7-14 are now expressed in then-current dollars (with annual inflation rate of 4%) in Table 7-13. The market interest rate reflecting this inflation is now 15%. In considering these expenses and receipts in then-current dollars and using an interest rate of 15% including inflation, we can recompute the cumulative net cash flow (with interest). Thus, the gross profit less financing costs becomes

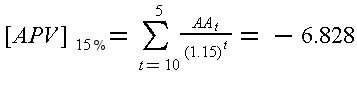

Example 7-17: Effects of Work Stoppage at Periods of Inflation Suppose further that besides the inflation rate of 4%, the project in

Example 7-16 is suspended at the end of year 2 due to a labor strike and

resumed after one year. Also, assume that while the contractor will incur

higher interest expenses due to the work stoppage, the owner will not

increase the payments to the contractor. The cumulative net cash flows

for the cases of operation and financing expenses are recomputed and tabulated

in Table 7-14. The construction expenses and receipts in then-current

dollars resulting from the work stopping and the corresponding net cash

flow of the project including financing (with annual interest accumulated

in the overdraft to the end of the project) is shown in Fig. 7-3. It is

noteworthy that, with or without the work stoppage, the gross operating

profit declines in value at the end of the project as a result of inflation,

but with the work stoppage it has eroded - further to a loss of $3.524

million as indicated by

Figure 7-3 Effects of Inflation and Work Stoppage Back to top 7.11 References

7.12 Problems

7.13 Footnotes1. This table is adapted from A.J. Henkel, "The Mechanics of a Revenue Bond Financing: An Overview," Infrastructure Financing, Kidder, Peabody & Co., New York, 1984. (Back) 2. The calculations for this bond issue are adapted from a hypothetical example in F. H. Fuller, "Analyzing Cash Flows for Revenue Bond Financing," Infrastructure Financing, Kidder, Peabody & Co., Inc., New York, 1984, pp. 37-47. (Back) 3. Maevis, Alfred C.,"Construction Cost Control by the

Owner," ASCE Journal of the Construction Division, Vol. 106, No.

4, December, 1980, pg. 444. (Back)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|